Posts

AI Automation is the New Industrial Revolution

Our AI investment thesis from 2020.

Jay Zhao

Sep 2, 2020

For a long time, I’ve had this old poster that illustrates the mechanics of the first steam engine in my office. One might wonder what a steam engine has to do with the “groundbreaking” technology companies a VC gets to interact with. The answer is “drastic productivity improvement.” The poster helps remind me that each tech breakthrough unleashes a tremendous amount of productivity — thus, value and wealth — within society. Like how the industrial revolution freed up labor and accelerated production, the age of AI automation is going to generate significant value for humanity in multiple ways.

Why AI Automation Matters Now

The term AI is not new. It originated in the 1960s as a field of computer science. However, the real breakthroughs came within the last decade when we developed new algorithms/techniques, including machine learning (ML, a subset of AI) and deep learning (a subset of ML), and later newer techniques like reinforcement learning, and transfer Learning. These new algorithms, coupled with an abundant amount of data for training, cloud computing, and sophisticated advancements of hardware AI chips, we are seeing highly valuable tech products being created every day based on such breakthroughs.

AI automation can materialize itself into multiple forms of products:

1) New products/category. Examples include self-driving cars, voice-enabled IoT, etc. Without AI being the backbone, we wouldn’t be able to enjoy these products;

2) Help with existing products’ scalability. Chatbots, virtual executive assistants, and face/image recognition would be in this category. It’s the territory where we used to have products in place but were either a) rule-based or b) man-powered and not scalable;

3) Inject efficiency and efficacy into software products. This is the category I’m most excited about as it will have profound implications for both B2B software / SaaS and enterprise customers across multiple industries and verticals. Think high-accuracy fraud detection, robotics/ smart manufacturing, predictive maintenance, intelligent business insight, etc.

What Has Happened

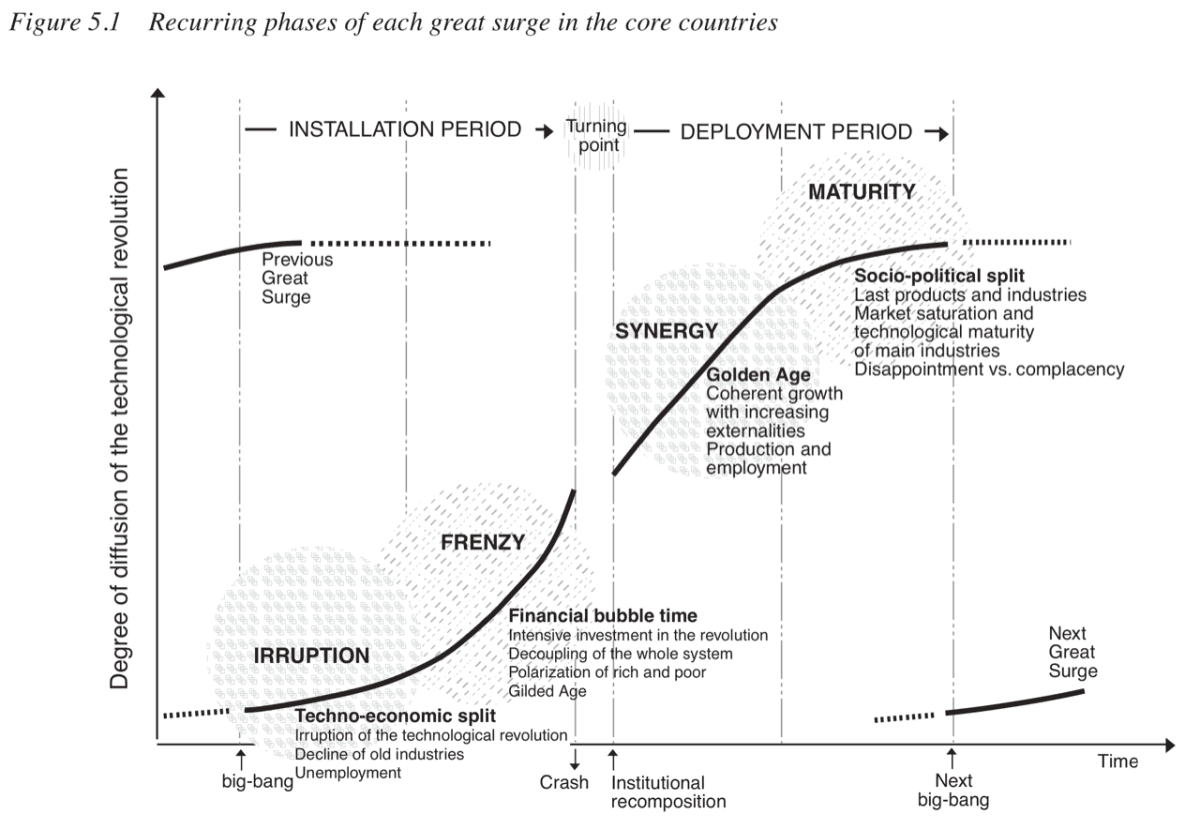

Through the framework of Carlota Perez in Technological Revolutions and Financial Capital (2002), we are witnessing AI companies cautiously transitioning from the “frenzy” stage to “synergy” and to the eventual “widespread application maturity” stage. Over the past five years, through the frenzy, investors have rushed into the AI space without thinking too deeply about the technology life cycle. Speculative capital has pushed up both the asset price and the expectation of many of the not-yet-ready AI companies. Namely, we have funded many self-driving cars/trucks/tractors and the related sensor components, but few can claim victory just yet. The abundance of capital inevitably diminishes the upside return and typically distracts startups from solving a real market need.

We are now experiencing a reckoning in the broad AI space, which results in several institutional adjustments through this critical “turning point.” And it’s healthy – just like a devasting fire in the forest often gives birth to a new ecosystem that is robust, the “turning point” provides the new default technology and the associated expectations to a breed of AI-first companies that focuses on solving real market needs in a capital-efficient manner. Nothing dissimilar to how the dot-com burst cleared the way for Amazon, Google, and the emerging Facebook, while wiping out companies like Pets.com, Webvan, and TheGlobe.com.

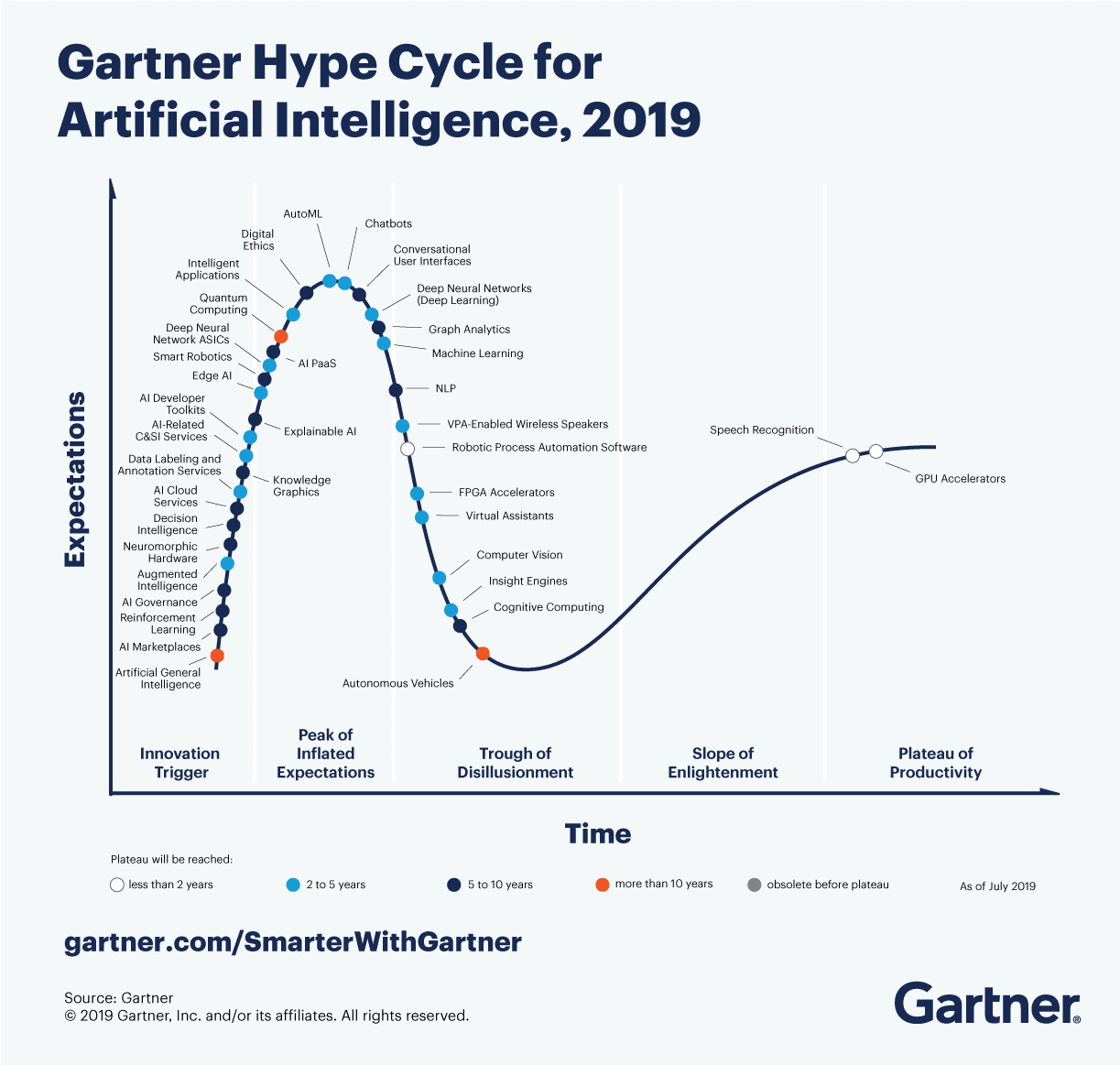

Looking out for the next decade, we are at a very interesting stage of time in the AI space. Recognizing the tech life cycle can help investors with long-term conviction capture some of the highest returns. The exact timing, of course, is hard to predict. Gartner Hype Cycle offers a rough overview of the timing of various subcategories of AI technology, which is somewhat consistent with the state of the AI life cycle portrayed by Perez.

In any case, the macro trend of AI automation is not going away.* And it’s going to boost humanity’s productivity to the next level.

Characteristics of the New “AI-First” Species

What the new AI automation presents is a unique landscape shift that will make many incumbents struggle to adopt. On the other hand, it will also give rise to many “new species"** companies that are AI-first.

The last few times when major landscape shifts took place, we have had “new species” rise in response to the new world. Think Industrialization (Ford Motors), Computer (IBM, Intel, Apple, Microsoft), Internet / Cloud / Mobile (Salesforce, Amazon, Google, Facebook). Iconic companies were created when they can ride major tech tides.

This time is no different. Except the unleashed productivity will likely be in the trillions of trillions of dollars, and the impact will last centuries. That’s why we need to study and take a closer look at the early characteristics of these “AI-first” companies – the new type of species that they are.

Just like any emergence of new species in mother nature, AI-first companies, although share some common traits with traditional software/SaaS counterparts, carry very different characteristics. More interestingly, the new species behave, in many ways, more aggressively than the incumbents.

We will examine a few intriguing aspects of this AI-first species: from the gross margin, product form, and business moat, to ultimately the billion-dollar question – how do we adequately measure the size (value) of these AI-first companies?

Let’s first look at some unusual characteristics of these AI-first companies.

1) Unlike typical software companies, the “AI-first” companies might have a non-software-like low margin (at first). And it might be a good thing.

Investors love the 80% margin business. So do traditional software companies. Over the last decades, we have seen powerful high-margin software companies – such as Salesforce, Oracle, and SAP – create and dominate their respective fields for a long time. One of the advantages of having a high-margin product is that it allows you to stack up on your well-oiled go-to-market machine continuously. In other words, it enables the incumbents to be extremely good at doing what they have been doing. And it’s a comfortable situation.

For the new species of “AI-first” companies, they wear the cover of “low margin,” at least initially, to enter different business territories. And this is not by choice. It’s the embedded nature of AI companies at its initial phase for the following two reasons:

a) In the field of AI, it’s easy to get to 80% accuracy; it takes investment and resources to get to 95%, but it’s near impossible to get to 100% because of the diminishing returns of solving the last 5% edge cases. Because of such dynamics, AI companies still employ humans on two fronts – data labeling/training and edge-case solving. And these humans are often data scientists who are not cheap. The cost of such eats away margins.

b) Contrary to popular belief, AI computing actually costs more than the traditional one, especially as more training data accumulates *and* as your algorithm is getting more complicated. Ironically, AI companies’ cloud computing costs are likely to be much higher as the business becomes more successful. And this is not even counting the often-ignored fact that AI companies, unlike traditional software ones, will need to retrain or “refresh” their data algorithms periodically to reflect the latest reality (e.g., mapping data, latest business wording, etc.).

It’s worth noting that both constraints above are not unsolvable, especially as we make more progress on the improvement of AI-computing infrastructure. It will just take some time. Therefore, these AI-first companies will usually carry a non-attractive low margin, at least initially.

Believe it or not, this might be a good thing, which leads me to my second point.

2) “AI-first” species’ low margin is its deceptive camouflage. Underneath, it is often a highly attractive ROI solution or service. It should get incumbents worried.

As Clayton Christensen – author of the classic book “Innovators’ Dilemma” – points out, disruptive new entrants usually come in the form of “non-attractive low margin” business that’s “easy to ignore.” Such dynamics happened when the minicomputer (DEC, Wang, etc.) disrupted mainframe computers (mostly IBM), and then quickly the personal computer (Microsoft, Apple, etc.) made the minicomputer obsolete. In both cases, the emergence of the minicomputer and PC came with audiences that were rather niche but were proliferating nonetheless.

The nature of a “niche” market made the “customer-driven” incumbents turn their heads sideways because their main customer base didn’t demand either minicomputer or PC at the time. More importantly, the “low margin” characteristics of the new entrants essentially stripped incumbents’ incentives to be “lean” and to be innovative again.***

Now with such a framework in mind. Let’s look at what’s happening now.

AI-first companies are attacking new territories and replacing older software in the same way as the PC era illustrates. Yet AI-first companies are making the moves more aggressively in a pattern we have rarely seen before. So it’s incredibly tricky and dangerous for incumbent tech companies on two fronts:

a) Unlike traditional software companies that usually offer one specific value (i.e., Salesforce for CRM, Box for storage, etc.), a robust AI-first company might propose itself as a full-service company with better ROI for customers. For example, we have seen AI companies “disguise” as a virtual lead-gen / sales force service agency that could potentially replace companies’ in-house business development or sales staff. Under the hood of these “service” companies, most of the operations are automated through AI. Therefore, it results in lower monthly costs to the customers, even though the initial COGS might be higher than that of AI-first companies.

On top of that, it would be easier to match sales/lead gen performance against the cost: it’s not hard for an executive to choose $100K on sales staff vs. a $20K “service” fee for this AI solution. Other territories that are being disrupted are customer service/call centers, executive assistants/scheduling, and legal document review/compliance, just to name a few.

The customers who are responding well and quickly are often the ones who value cost-efficiency the most. They are usually startups and SMBs. They are AI-first companies’ first “nitch market” that is often underserved (and overcharged) by incumbents. They are the beachheads.

By establishing an ultra-strong ROI case on a particular business function (i.e., sales, call center, EA, etc.), AI-first companies are quickly building up the beachheads before attacking incumbents’ primary market – Fortune 500 customers.

b) On the incumbents’ side, the existing high-margin software business offers little incentive to explore AI-service-like products with a lower margin. More importantly, much of the incumbents’ existing customer base – the stable large-cap companies – might be willing to try out some AI-first products, but they do not demand them.

Why?

First, the mainstream market, by definition, is conservative and usually likes to wait until fully adopt a new product. Second, thanks to software incumbents’ decade-long effort in building high-switching costs to their products, the customers are even less likely to be proactively looking for new solutions.

Therefore, the “conservative” customer base, plus the high margin “lifestyle,” will immobilize incumbents to react and defend against the inevitable take-over from the new breed of AI-first companies. Such is life.

However, this is not to say that AI-first companies don’t have shortcomings. Other than the “low margin” factor as mentioned above, AI companies will have to figure out a few things, including the sustainability of the moat. This lead to my third point.

3) Unlike typical social network or marketplace companies, the moat for “AI-first” companies might not be deep. Therefore, the initial data advantage and an ongoing low-cost data acquisition would be the key.

Because AI algorithms are widely open-sourced, the keys to building a defensible business are proprietary data and the method of keeping acquiring quality data cheaply.****

Because of such dynamics, it’s not hard to foresee the successful breed of AI-first companies will be heavily vertical-integrated and even service-oriented (at first). Therefore, there won’t be such a thing as horizontal AI (with the exception that maybe Alphabet or Microsoft can morph into horizontal AI players). Instead, we will be seeing AI companies build their data pools, users, and brands in specific verticals such as healthcare, payment, media, automotive, and manufacturing.

We are still in the early days. I don’t think we have to figure out the best practices for obtaining sustainable data moat yet.

On the one hand, it could be a capital-intensive endeavor as we have seen Google/Waymo invest billions in its self-driving AI as it keeps updating the mapping and driving data on its own. On the other hand, we have seen some startups being creative by striking partnerships with hospitals, payment processors, and OEMs to get the initial data advantage started. However, is either approach sustainable and scalable? We don’t know. We haven’t figured out the formulas as much as we have on many of the SaaS calculations.

One might imagine a very different pricing model that is offered by AI companies. We have discussed that AI-first companies might charge customers on a service basis (initially). But the pricing model might eventually mutate into data-discounted pricing where the customers might enjoy much of the discount in exchange for the training data they contribute. So that would be very different than the typical SaaS companies’ per-seat model.

The Next Mega-Giants

How do we, the investors, properly evaluate these pricing models and the underlying business created by this new breed of “AI-first” companies?

I would expect it to be different from a typical Cloud/ SaaS multiple, likely higher. My guess: in the coming ten years, we will be witnessing a new breed of tech companies that are much more automated, intelligent, and ever more embedded in business functions. And this unleashes significant values.

The market valuation for these AI-first companies will likely be much higher than the “1-billion-dollar unicorns” over the next decade – we are likely to see a few trillion-dollar companies across the US and China. What would be the AI-first equivalents of Amazon, Apple, and Alibaba? What would be the AI-first incumbents in mega markets such as enterprise software, healthcare, and industrial?

Don Valentine, the founder of Sequoia Capital, insisted that in looking for great companies, the key is to identify huge markets and study the competitive dynamics within them. That’s how Sequoia has consistently backed category-defining companies from Apple to Cisco, to Yahoo, to Google, to Whatsapp, to Zoom. There is truth to that. Successful companies often do not create value by merely introducing groundbreaking technologies but rather by solving pain points in large enough markets. So building a successful AI-first company is more about solving the GTM marketing problem, rather than a technology one.

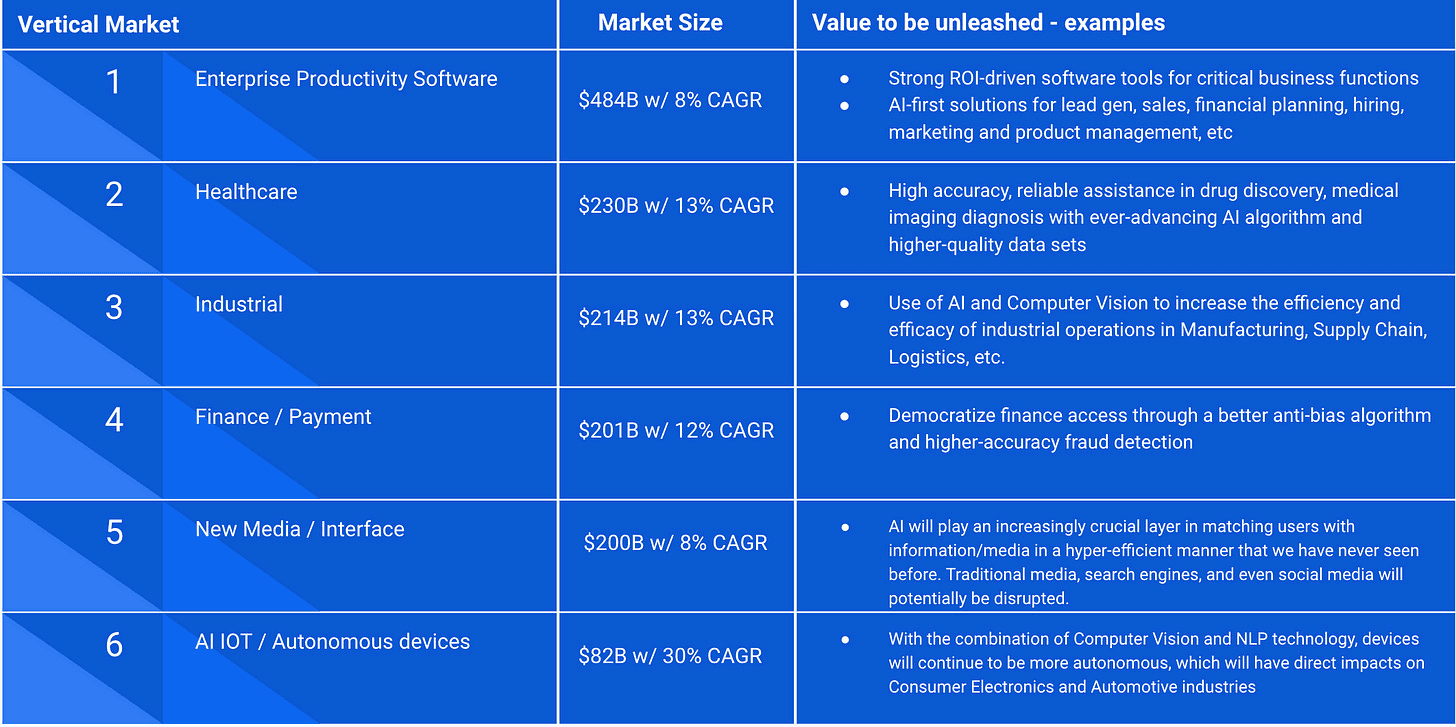

The following 6 markets are mostly above $200B and continue to grow at 10%+ annually. The enablement of AI will unleash newfound values within these markets and in some cases, cause major disruptions of the existing monopolistic-like dynamics.

Take the media space for example, the emergence of ByteDance is only the beginning. It proves that a strong AI has the capability of turning the traditional market upside down – in this case, it reverts the century-long process of “humans look for relevant information” to “relevant information comes to humans.” This is just scratching the surface. And yet the incumbents’ companies like Google and Facebook should be very concerned as innovations in this area would very well disrupt the existing order of social media and search engine spaces, to the very least.

If history is of any guidance, we should be well prepared by studying the trend and then embracingit fully.

* In many cases, it’s accelerated by recent events such as the pandemic.

**As strange as it might sound, when I was a kid, I was fascinated by Darwin’s book “On the Origin of Species.” The work not only lays out how animals adapt to a new environment, but it also paints competitive dynamics between the old and emerging species that lead to such adoption/evolution. Even as an adult, I still love books and documentaries about nature.

It absolutely delighted me when I find out how similar it is between nature and our business world – i.e. bio-ecosystem VS market dynamics, landscape shift VS new tech breakthroughs, startups and incumbents VS new and old species. How the business world evolves is really not that much different than our mother nature.

*** Another example would be Netflix vs. traditional media companies. Started as a DVD rental business (i.e., you actually have to mail out physical DVDs and then expect consumers to mail them back via the US Postal Office), Netflix’s original business model was heavy with DVD warehouse and intense sorting and mailing labor operation, thus, arelatively low margin business. Because of the initial “low margin” characteristic, many media senior executives were blindsided. The gravity of short-term quarterly profit pulled them away from the long-term threat of Netflix. Many in the media industry failed to imagine how Netflix could morph into a digital-first streaming product that left giants such as Disney and Warner to play catch-up.

**** This is assuming everything else is equal. It’s worthwhile to point out that compared to traditional software companies, AI-first companies might have to be better at sales and marketing as the customer market will experience a learning curve on its own. Within the AI companies – which are often staffed with engineers and data scientists — the ones who have the best GTM approach /team will dominate since the end market doesn’t care about the technology but rather the ROI-proven solutions.

For a long time, I’ve had this old poster that illustrates the mechanics of the first steam engine in my office. One might wonder what a steam engine has to do with the “groundbreaking” technology companies a VC gets to interact with. The answer is “drastic productivity improvement.” The poster helps remind me that each tech breakthrough unleashes a tremendous amount of productivity — thus, value and wealth — within society. Like how the industrial revolution freed up labor and accelerated production, the age of AI automation is going to generate significant value for humanity in multiple ways.

Why AI Automation Matters Now

The term AI is not new. It originated in the 1960s as a field of computer science. However, the real breakthroughs came within the last decade when we developed new algorithms/techniques, including machine learning (ML, a subset of AI) and deep learning (a subset of ML), and later newer techniques like reinforcement learning, and transfer Learning. These new algorithms, coupled with an abundant amount of data for training, cloud computing, and sophisticated advancements of hardware AI chips, we are seeing highly valuable tech products being created every day based on such breakthroughs.

AI automation can materialize itself into multiple forms of products:

1) New products/category. Examples include self-driving cars, voice-enabled IoT, etc. Without AI being the backbone, we wouldn’t be able to enjoy these products;

2) Help with existing products’ scalability. Chatbots, virtual executive assistants, and face/image recognition would be in this category. It’s the territory where we used to have products in place but were either a) rule-based or b) man-powered and not scalable;

3) Inject efficiency and efficacy into software products. This is the category I’m most excited about as it will have profound implications for both B2B software / SaaS and enterprise customers across multiple industries and verticals. Think high-accuracy fraud detection, robotics/ smart manufacturing, predictive maintenance, intelligent business insight, etc.

What Has Happened

Through the framework of Carlota Perez in Technological Revolutions and Financial Capital (2002), we are witnessing AI companies cautiously transitioning from the “frenzy” stage to “synergy” and to the eventual “widespread application maturity” stage. Over the past five years, through the frenzy, investors have rushed into the AI space without thinking too deeply about the technology life cycle. Speculative capital has pushed up both the asset price and the expectation of many of the not-yet-ready AI companies. Namely, we have funded many self-driving cars/trucks/tractors and the related sensor components, but few can claim victory just yet. The abundance of capital inevitably diminishes the upside return and typically distracts startups from solving a real market need.

We are now experiencing a reckoning in the broad AI space, which results in several institutional adjustments through this critical “turning point.” And it’s healthy – just like a devasting fire in the forest often gives birth to a new ecosystem that is robust, the “turning point” provides the new default technology and the associated expectations to a breed of AI-first companies that focuses on solving real market needs in a capital-efficient manner. Nothing dissimilar to how the dot-com burst cleared the way for Amazon, Google, and the emerging Facebook, while wiping out companies like Pets.com, Webvan, and TheGlobe.com.

Looking out for the next decade, we are at a very interesting stage of time in the AI space. Recognizing the tech life cycle can help investors with long-term conviction capture some of the highest returns. The exact timing, of course, is hard to predict. Gartner Hype Cycle offers a rough overview of the timing of various subcategories of AI technology, which is somewhat consistent with the state of the AI life cycle portrayed by Perez.

In any case, the macro trend of AI automation is not going away.* And it’s going to boost humanity’s productivity to the next level.

Characteristics of the New “AI-First” Species

What the new AI automation presents is a unique landscape shift that will make many incumbents struggle to adopt. On the other hand, it will also give rise to many “new species"** companies that are AI-first.

The last few times when major landscape shifts took place, we have had “new species” rise in response to the new world. Think Industrialization (Ford Motors), Computer (IBM, Intel, Apple, Microsoft), Internet / Cloud / Mobile (Salesforce, Amazon, Google, Facebook). Iconic companies were created when they can ride major tech tides.

This time is no different. Except the unleashed productivity will likely be in the trillions of trillions of dollars, and the impact will last centuries. That’s why we need to study and take a closer look at the early characteristics of these “AI-first” companies – the new type of species that they are.

Just like any emergence of new species in mother nature, AI-first companies, although share some common traits with traditional software/SaaS counterparts, carry very different characteristics. More interestingly, the new species behave, in many ways, more aggressively than the incumbents.

We will examine a few intriguing aspects of this AI-first species: from the gross margin, product form, and business moat, to ultimately the billion-dollar question – how do we adequately measure the size (value) of these AI-first companies?

Let’s first look at some unusual characteristics of these AI-first companies.

1) Unlike typical software companies, the “AI-first” companies might have a non-software-like low margin (at first). And it might be a good thing.

Investors love the 80% margin business. So do traditional software companies. Over the last decades, we have seen powerful high-margin software companies – such as Salesforce, Oracle, and SAP – create and dominate their respective fields for a long time. One of the advantages of having a high-margin product is that it allows you to stack up on your well-oiled go-to-market machine continuously. In other words, it enables the incumbents to be extremely good at doing what they have been doing. And it’s a comfortable situation.

For the new species of “AI-first” companies, they wear the cover of “low margin,” at least initially, to enter different business territories. And this is not by choice. It’s the embedded nature of AI companies at its initial phase for the following two reasons:

a) In the field of AI, it’s easy to get to 80% accuracy; it takes investment and resources to get to 95%, but it’s near impossible to get to 100% because of the diminishing returns of solving the last 5% edge cases. Because of such dynamics, AI companies still employ humans on two fronts – data labeling/training and edge-case solving. And these humans are often data scientists who are not cheap. The cost of such eats away margins.

b) Contrary to popular belief, AI computing actually costs more than the traditional one, especially as more training data accumulates *and* as your algorithm is getting more complicated. Ironically, AI companies’ cloud computing costs are likely to be much higher as the business becomes more successful. And this is not even counting the often-ignored fact that AI companies, unlike traditional software ones, will need to retrain or “refresh” their data algorithms periodically to reflect the latest reality (e.g., mapping data, latest business wording, etc.).

It’s worth noting that both constraints above are not unsolvable, especially as we make more progress on the improvement of AI-computing infrastructure. It will just take some time. Therefore, these AI-first companies will usually carry a non-attractive low margin, at least initially.

Believe it or not, this might be a good thing, which leads me to my second point.

2) “AI-first” species’ low margin is its deceptive camouflage. Underneath, it is often a highly attractive ROI solution or service. It should get incumbents worried.

As Clayton Christensen – author of the classic book “Innovators’ Dilemma” – points out, disruptive new entrants usually come in the form of “non-attractive low margin” business that’s “easy to ignore.” Such dynamics happened when the minicomputer (DEC, Wang, etc.) disrupted mainframe computers (mostly IBM), and then quickly the personal computer (Microsoft, Apple, etc.) made the minicomputer obsolete. In both cases, the emergence of the minicomputer and PC came with audiences that were rather niche but were proliferating nonetheless.

The nature of a “niche” market made the “customer-driven” incumbents turn their heads sideways because their main customer base didn’t demand either minicomputer or PC at the time. More importantly, the “low margin” characteristics of the new entrants essentially stripped incumbents’ incentives to be “lean” and to be innovative again.***

Now with such a framework in mind. Let’s look at what’s happening now.

AI-first companies are attacking new territories and replacing older software in the same way as the PC era illustrates. Yet AI-first companies are making the moves more aggressively in a pattern we have rarely seen before. So it’s incredibly tricky and dangerous for incumbent tech companies on two fronts:

a) Unlike traditional software companies that usually offer one specific value (i.e., Salesforce for CRM, Box for storage, etc.), a robust AI-first company might propose itself as a full-service company with better ROI for customers. For example, we have seen AI companies “disguise” as a virtual lead-gen / sales force service agency that could potentially replace companies’ in-house business development or sales staff. Under the hood of these “service” companies, most of the operations are automated through AI. Therefore, it results in lower monthly costs to the customers, even though the initial COGS might be higher than that of AI-first companies.

On top of that, it would be easier to match sales/lead gen performance against the cost: it’s not hard for an executive to choose $100K on sales staff vs. a $20K “service” fee for this AI solution. Other territories that are being disrupted are customer service/call centers, executive assistants/scheduling, and legal document review/compliance, just to name a few.

The customers who are responding well and quickly are often the ones who value cost-efficiency the most. They are usually startups and SMBs. They are AI-first companies’ first “nitch market” that is often underserved (and overcharged) by incumbents. They are the beachheads.

By establishing an ultra-strong ROI case on a particular business function (i.e., sales, call center, EA, etc.), AI-first companies are quickly building up the beachheads before attacking incumbents’ primary market – Fortune 500 customers.

b) On the incumbents’ side, the existing high-margin software business offers little incentive to explore AI-service-like products with a lower margin. More importantly, much of the incumbents’ existing customer base – the stable large-cap companies – might be willing to try out some AI-first products, but they do not demand them.

Why?

First, the mainstream market, by definition, is conservative and usually likes to wait until fully adopt a new product. Second, thanks to software incumbents’ decade-long effort in building high-switching costs to their products, the customers are even less likely to be proactively looking for new solutions.

Therefore, the “conservative” customer base, plus the high margin “lifestyle,” will immobilize incumbents to react and defend against the inevitable take-over from the new breed of AI-first companies. Such is life.

However, this is not to say that AI-first companies don’t have shortcomings. Other than the “low margin” factor as mentioned above, AI companies will have to figure out a few things, including the sustainability of the moat. This lead to my third point.

3) Unlike typical social network or marketplace companies, the moat for “AI-first” companies might not be deep. Therefore, the initial data advantage and an ongoing low-cost data acquisition would be the key.

Because AI algorithms are widely open-sourced, the keys to building a defensible business are proprietary data and the method of keeping acquiring quality data cheaply.****

Because of such dynamics, it’s not hard to foresee the successful breed of AI-first companies will be heavily vertical-integrated and even service-oriented (at first). Therefore, there won’t be such a thing as horizontal AI (with the exception that maybe Alphabet or Microsoft can morph into horizontal AI players). Instead, we will be seeing AI companies build their data pools, users, and brands in specific verticals such as healthcare, payment, media, automotive, and manufacturing.

We are still in the early days. I don’t think we have to figure out the best practices for obtaining sustainable data moat yet.

On the one hand, it could be a capital-intensive endeavor as we have seen Google/Waymo invest billions in its self-driving AI as it keeps updating the mapping and driving data on its own. On the other hand, we have seen some startups being creative by striking partnerships with hospitals, payment processors, and OEMs to get the initial data advantage started. However, is either approach sustainable and scalable? We don’t know. We haven’t figured out the formulas as much as we have on many of the SaaS calculations.

One might imagine a very different pricing model that is offered by AI companies. We have discussed that AI-first companies might charge customers on a service basis (initially). But the pricing model might eventually mutate into data-discounted pricing where the customers might enjoy much of the discount in exchange for the training data they contribute. So that would be very different than the typical SaaS companies’ per-seat model.

The Next Mega-Giants

How do we, the investors, properly evaluate these pricing models and the underlying business created by this new breed of “AI-first” companies?

I would expect it to be different from a typical Cloud/ SaaS multiple, likely higher. My guess: in the coming ten years, we will be witnessing a new breed of tech companies that are much more automated, intelligent, and ever more embedded in business functions. And this unleashes significant values.

The market valuation for these AI-first companies will likely be much higher than the “1-billion-dollar unicorns” over the next decade – we are likely to see a few trillion-dollar companies across the US and China. What would be the AI-first equivalents of Amazon, Apple, and Alibaba? What would be the AI-first incumbents in mega markets such as enterprise software, healthcare, and industrial?

Don Valentine, the founder of Sequoia Capital, insisted that in looking for great companies, the key is to identify huge markets and study the competitive dynamics within them. That’s how Sequoia has consistently backed category-defining companies from Apple to Cisco, to Yahoo, to Google, to Whatsapp, to Zoom. There is truth to that. Successful companies often do not create value by merely introducing groundbreaking technologies but rather by solving pain points in large enough markets. So building a successful AI-first company is more about solving the GTM marketing problem, rather than a technology one.

The following 6 markets are mostly above $200B and continue to grow at 10%+ annually. The enablement of AI will unleash newfound values within these markets and in some cases, cause major disruptions of the existing monopolistic-like dynamics.

Take the media space for example, the emergence of ByteDance is only the beginning. It proves that a strong AI has the capability of turning the traditional market upside down – in this case, it reverts the century-long process of “humans look for relevant information” to “relevant information comes to humans.” This is just scratching the surface. And yet the incumbents’ companies like Google and Facebook should be very concerned as innovations in this area would very well disrupt the existing order of social media and search engine spaces, to the very least.

If history is of any guidance, we should be well prepared by studying the trend and then embracingit fully.

* In many cases, it’s accelerated by recent events such as the pandemic.

**As strange as it might sound, when I was a kid, I was fascinated by Darwin’s book “On the Origin of Species.” The work not only lays out how animals adapt to a new environment, but it also paints competitive dynamics between the old and emerging species that lead to such adoption/evolution. Even as an adult, I still love books and documentaries about nature.

It absolutely delighted me when I find out how similar it is between nature and our business world – i.e. bio-ecosystem VS market dynamics, landscape shift VS new tech breakthroughs, startups and incumbents VS new and old species. How the business world evolves is really not that much different than our mother nature.

*** Another example would be Netflix vs. traditional media companies. Started as a DVD rental business (i.e., you actually have to mail out physical DVDs and then expect consumers to mail them back via the US Postal Office), Netflix’s original business model was heavy with DVD warehouse and intense sorting and mailing labor operation, thus, arelatively low margin business. Because of the initial “low margin” characteristic, many media senior executives were blindsided. The gravity of short-term quarterly profit pulled them away from the long-term threat of Netflix. Many in the media industry failed to imagine how Netflix could morph into a digital-first streaming product that left giants such as Disney and Warner to play catch-up.

**** This is assuming everything else is equal. It’s worthwhile to point out that compared to traditional software companies, AI-first companies might have to be better at sales and marketing as the customer market will experience a learning curve on its own. Within the AI companies – which are often staffed with engineers and data scientists — the ones who have the best GTM approach /team will dominate since the end market doesn’t care about the technology but rather the ROI-proven solutions.

For a long time, I’ve had this old poster that illustrates the mechanics of the first steam engine in my office. One might wonder what a steam engine has to do with the “groundbreaking” technology companies a VC gets to interact with. The answer is “drastic productivity improvement.” The poster helps remind me that each tech breakthrough unleashes a tremendous amount of productivity — thus, value and wealth — within society. Like how the industrial revolution freed up labor and accelerated production, the age of AI automation is going to generate significant value for humanity in multiple ways.

Why AI Automation Matters Now

The term AI is not new. It originated in the 1960s as a field of computer science. However, the real breakthroughs came within the last decade when we developed new algorithms/techniques, including machine learning (ML, a subset of AI) and deep learning (a subset of ML), and later newer techniques like reinforcement learning, and transfer Learning. These new algorithms, coupled with an abundant amount of data for training, cloud computing, and sophisticated advancements of hardware AI chips, we are seeing highly valuable tech products being created every day based on such breakthroughs.

AI automation can materialize itself into multiple forms of products:

1) New products/category. Examples include self-driving cars, voice-enabled IoT, etc. Without AI being the backbone, we wouldn’t be able to enjoy these products;

2) Help with existing products’ scalability. Chatbots, virtual executive assistants, and face/image recognition would be in this category. It’s the territory where we used to have products in place but were either a) rule-based or b) man-powered and not scalable;

3) Inject efficiency and efficacy into software products. This is the category I’m most excited about as it will have profound implications for both B2B software / SaaS and enterprise customers across multiple industries and verticals. Think high-accuracy fraud detection, robotics/ smart manufacturing, predictive maintenance, intelligent business insight, etc.

What Has Happened

Through the framework of Carlota Perez in Technological Revolutions and Financial Capital (2002), we are witnessing AI companies cautiously transitioning from the “frenzy” stage to “synergy” and to the eventual “widespread application maturity” stage. Over the past five years, through the frenzy, investors have rushed into the AI space without thinking too deeply about the technology life cycle. Speculative capital has pushed up both the asset price and the expectation of many of the not-yet-ready AI companies. Namely, we have funded many self-driving cars/trucks/tractors and the related sensor components, but few can claim victory just yet. The abundance of capital inevitably diminishes the upside return and typically distracts startups from solving a real market need.

We are now experiencing a reckoning in the broad AI space, which results in several institutional adjustments through this critical “turning point.” And it’s healthy – just like a devasting fire in the forest often gives birth to a new ecosystem that is robust, the “turning point” provides the new default technology and the associated expectations to a breed of AI-first companies that focuses on solving real market needs in a capital-efficient manner. Nothing dissimilar to how the dot-com burst cleared the way for Amazon, Google, and the emerging Facebook, while wiping out companies like Pets.com, Webvan, and TheGlobe.com.

Looking out for the next decade, we are at a very interesting stage of time in the AI space. Recognizing the tech life cycle can help investors with long-term conviction capture some of the highest returns. The exact timing, of course, is hard to predict. Gartner Hype Cycle offers a rough overview of the timing of various subcategories of AI technology, which is somewhat consistent with the state of the AI life cycle portrayed by Perez.

In any case, the macro trend of AI automation is not going away.* And it’s going to boost humanity’s productivity to the next level.

Characteristics of the New “AI-First” Species

What the new AI automation presents is a unique landscape shift that will make many incumbents struggle to adopt. On the other hand, it will also give rise to many “new species"** companies that are AI-first.

The last few times when major landscape shifts took place, we have had “new species” rise in response to the new world. Think Industrialization (Ford Motors), Computer (IBM, Intel, Apple, Microsoft), Internet / Cloud / Mobile (Salesforce, Amazon, Google, Facebook). Iconic companies were created when they can ride major tech tides.

This time is no different. Except the unleashed productivity will likely be in the trillions of trillions of dollars, and the impact will last centuries. That’s why we need to study and take a closer look at the early characteristics of these “AI-first” companies – the new type of species that they are.

Just like any emergence of new species in mother nature, AI-first companies, although share some common traits with traditional software/SaaS counterparts, carry very different characteristics. More interestingly, the new species behave, in many ways, more aggressively than the incumbents.

We will examine a few intriguing aspects of this AI-first species: from the gross margin, product form, and business moat, to ultimately the billion-dollar question – how do we adequately measure the size (value) of these AI-first companies?

Let’s first look at some unusual characteristics of these AI-first companies.

1) Unlike typical software companies, the “AI-first” companies might have a non-software-like low margin (at first). And it might be a good thing.

Investors love the 80% margin business. So do traditional software companies. Over the last decades, we have seen powerful high-margin software companies – such as Salesforce, Oracle, and SAP – create and dominate their respective fields for a long time. One of the advantages of having a high-margin product is that it allows you to stack up on your well-oiled go-to-market machine continuously. In other words, it enables the incumbents to be extremely good at doing what they have been doing. And it’s a comfortable situation.

For the new species of “AI-first” companies, they wear the cover of “low margin,” at least initially, to enter different business territories. And this is not by choice. It’s the embedded nature of AI companies at its initial phase for the following two reasons:

a) In the field of AI, it’s easy to get to 80% accuracy; it takes investment and resources to get to 95%, but it’s near impossible to get to 100% because of the diminishing returns of solving the last 5% edge cases. Because of such dynamics, AI companies still employ humans on two fronts – data labeling/training and edge-case solving. And these humans are often data scientists who are not cheap. The cost of such eats away margins.

b) Contrary to popular belief, AI computing actually costs more than the traditional one, especially as more training data accumulates *and* as your algorithm is getting more complicated. Ironically, AI companies’ cloud computing costs are likely to be much higher as the business becomes more successful. And this is not even counting the often-ignored fact that AI companies, unlike traditional software ones, will need to retrain or “refresh” their data algorithms periodically to reflect the latest reality (e.g., mapping data, latest business wording, etc.).

It’s worth noting that both constraints above are not unsolvable, especially as we make more progress on the improvement of AI-computing infrastructure. It will just take some time. Therefore, these AI-first companies will usually carry a non-attractive low margin, at least initially.

Believe it or not, this might be a good thing, which leads me to my second point.

2) “AI-first” species’ low margin is its deceptive camouflage. Underneath, it is often a highly attractive ROI solution or service. It should get incumbents worried.

As Clayton Christensen – author of the classic book “Innovators’ Dilemma” – points out, disruptive new entrants usually come in the form of “non-attractive low margin” business that’s “easy to ignore.” Such dynamics happened when the minicomputer (DEC, Wang, etc.) disrupted mainframe computers (mostly IBM), and then quickly the personal computer (Microsoft, Apple, etc.) made the minicomputer obsolete. In both cases, the emergence of the minicomputer and PC came with audiences that were rather niche but were proliferating nonetheless.

The nature of a “niche” market made the “customer-driven” incumbents turn their heads sideways because their main customer base didn’t demand either minicomputer or PC at the time. More importantly, the “low margin” characteristics of the new entrants essentially stripped incumbents’ incentives to be “lean” and to be innovative again.***

Now with such a framework in mind. Let’s look at what’s happening now.

AI-first companies are attacking new territories and replacing older software in the same way as the PC era illustrates. Yet AI-first companies are making the moves more aggressively in a pattern we have rarely seen before. So it’s incredibly tricky and dangerous for incumbent tech companies on two fronts:

a) Unlike traditional software companies that usually offer one specific value (i.e., Salesforce for CRM, Box for storage, etc.), a robust AI-first company might propose itself as a full-service company with better ROI for customers. For example, we have seen AI companies “disguise” as a virtual lead-gen / sales force service agency that could potentially replace companies’ in-house business development or sales staff. Under the hood of these “service” companies, most of the operations are automated through AI. Therefore, it results in lower monthly costs to the customers, even though the initial COGS might be higher than that of AI-first companies.

On top of that, it would be easier to match sales/lead gen performance against the cost: it’s not hard for an executive to choose $100K on sales staff vs. a $20K “service” fee for this AI solution. Other territories that are being disrupted are customer service/call centers, executive assistants/scheduling, and legal document review/compliance, just to name a few.

The customers who are responding well and quickly are often the ones who value cost-efficiency the most. They are usually startups and SMBs. They are AI-first companies’ first “nitch market” that is often underserved (and overcharged) by incumbents. They are the beachheads.

By establishing an ultra-strong ROI case on a particular business function (i.e., sales, call center, EA, etc.), AI-first companies are quickly building up the beachheads before attacking incumbents’ primary market – Fortune 500 customers.

b) On the incumbents’ side, the existing high-margin software business offers little incentive to explore AI-service-like products with a lower margin. More importantly, much of the incumbents’ existing customer base – the stable large-cap companies – might be willing to try out some AI-first products, but they do not demand them.

Why?

First, the mainstream market, by definition, is conservative and usually likes to wait until fully adopt a new product. Second, thanks to software incumbents’ decade-long effort in building high-switching costs to their products, the customers are even less likely to be proactively looking for new solutions.

Therefore, the “conservative” customer base, plus the high margin “lifestyle,” will immobilize incumbents to react and defend against the inevitable take-over from the new breed of AI-first companies. Such is life.

However, this is not to say that AI-first companies don’t have shortcomings. Other than the “low margin” factor as mentioned above, AI companies will have to figure out a few things, including the sustainability of the moat. This lead to my third point.

3) Unlike typical social network or marketplace companies, the moat for “AI-first” companies might not be deep. Therefore, the initial data advantage and an ongoing low-cost data acquisition would be the key.

Because AI algorithms are widely open-sourced, the keys to building a defensible business are proprietary data and the method of keeping acquiring quality data cheaply.****

Because of such dynamics, it’s not hard to foresee the successful breed of AI-first companies will be heavily vertical-integrated and even service-oriented (at first). Therefore, there won’t be such a thing as horizontal AI (with the exception that maybe Alphabet or Microsoft can morph into horizontal AI players). Instead, we will be seeing AI companies build their data pools, users, and brands in specific verticals such as healthcare, payment, media, automotive, and manufacturing.

We are still in the early days. I don’t think we have to figure out the best practices for obtaining sustainable data moat yet.

On the one hand, it could be a capital-intensive endeavor as we have seen Google/Waymo invest billions in its self-driving AI as it keeps updating the mapping and driving data on its own. On the other hand, we have seen some startups being creative by striking partnerships with hospitals, payment processors, and OEMs to get the initial data advantage started. However, is either approach sustainable and scalable? We don’t know. We haven’t figured out the formulas as much as we have on many of the SaaS calculations.

One might imagine a very different pricing model that is offered by AI companies. We have discussed that AI-first companies might charge customers on a service basis (initially). But the pricing model might eventually mutate into data-discounted pricing where the customers might enjoy much of the discount in exchange for the training data they contribute. So that would be very different than the typical SaaS companies’ per-seat model.

The Next Mega-Giants

How do we, the investors, properly evaluate these pricing models and the underlying business created by this new breed of “AI-first” companies?

I would expect it to be different from a typical Cloud/ SaaS multiple, likely higher. My guess: in the coming ten years, we will be witnessing a new breed of tech companies that are much more automated, intelligent, and ever more embedded in business functions. And this unleashes significant values.

The market valuation for these AI-first companies will likely be much higher than the “1-billion-dollar unicorns” over the next decade – we are likely to see a few trillion-dollar companies across the US and China. What would be the AI-first equivalents of Amazon, Apple, and Alibaba? What would be the AI-first incumbents in mega markets such as enterprise software, healthcare, and industrial?

Don Valentine, the founder of Sequoia Capital, insisted that in looking for great companies, the key is to identify huge markets and study the competitive dynamics within them. That’s how Sequoia has consistently backed category-defining companies from Apple to Cisco, to Yahoo, to Google, to Whatsapp, to Zoom. There is truth to that. Successful companies often do not create value by merely introducing groundbreaking technologies but rather by solving pain points in large enough markets. So building a successful AI-first company is more about solving the GTM marketing problem, rather than a technology one.

The following 6 markets are mostly above $200B and continue to grow at 10%+ annually. The enablement of AI will unleash newfound values within these markets and in some cases, cause major disruptions of the existing monopolistic-like dynamics.

Take the media space for example, the emergence of ByteDance is only the beginning. It proves that a strong AI has the capability of turning the traditional market upside down – in this case, it reverts the century-long process of “humans look for relevant information” to “relevant information comes to humans.” This is just scratching the surface. And yet the incumbents’ companies like Google and Facebook should be very concerned as innovations in this area would very well disrupt the existing order of social media and search engine spaces, to the very least.

If history is of any guidance, we should be well prepared by studying the trend and then embracingit fully.

* In many cases, it’s accelerated by recent events such as the pandemic.

**As strange as it might sound, when I was a kid, I was fascinated by Darwin’s book “On the Origin of Species.” The work not only lays out how animals adapt to a new environment, but it also paints competitive dynamics between the old and emerging species that lead to such adoption/evolution. Even as an adult, I still love books and documentaries about nature.

It absolutely delighted me when I find out how similar it is between nature and our business world – i.e. bio-ecosystem VS market dynamics, landscape shift VS new tech breakthroughs, startups and incumbents VS new and old species. How the business world evolves is really not that much different than our mother nature.

*** Another example would be Netflix vs. traditional media companies. Started as a DVD rental business (i.e., you actually have to mail out physical DVDs and then expect consumers to mail them back via the US Postal Office), Netflix’s original business model was heavy with DVD warehouse and intense sorting and mailing labor operation, thus, arelatively low margin business. Because of the initial “low margin” characteristic, many media senior executives were blindsided. The gravity of short-term quarterly profit pulled them away from the long-term threat of Netflix. Many in the media industry failed to imagine how Netflix could morph into a digital-first streaming product that left giants such as Disney and Warner to play catch-up.

**** This is assuming everything else is equal. It’s worthwhile to point out that compared to traditional software companies, AI-first companies might have to be better at sales and marketing as the customer market will experience a learning curve on its own. Within the AI companies – which are often staffed with engineers and data scientists — the ones who have the best GTM approach /team will dominate since the end market doesn’t care about the technology but rather the ROI-proven solutions.

Sign up for our newsletter

Sign up for our newsletter

Be the first to know about our industry trends and our research insights.

Be the first to know about our industry trends and our research insights.

Latest

From the blog

The latest industry news, interviews, technologies, and resources.

Leonis [leōnis]: Latin for “Lion Strength”. Alpha Leonis is one of the brightest and most enduring stars in the Leo star constellation.

Newsletter

Leonis [leōnis]: Latin for “Lion Strength”. Alpha Leonis is one of the brightest and most enduring stars in the Leo star constellation.

Newsletter

Leonis [leōnis]: Latin for “Lion Strength”. Alpha Leonis is one of the brightest and most enduring stars in the Leo star constellation.

Newsletter